Context

- The ongoing conflict in West Asia has disrupted global energy flows, affecting Liquefied Natural Gas (LNG) supply, which is a key input for urea production in India.

- This crisis highlights India’s dual dependence i.e. on imported LNG for domestic production and on West Asia for urea imports, making fertilizer security vulnerable to geopolitical shocks.

Key Data and Trends

- India imports over 50% of its natural gas requirements, making it highly exposed to global supply disruptions.

- India imported about 261 lakh metric tonnes of LNG in 2025, making it the fourth-largest global importer.

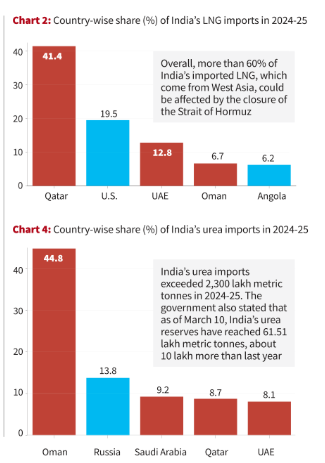

- More than 40% of LNG imports come from Qatar, with additional supplies from the UAE and Oman.

- Around 60% of India’s LNG imports pass through the Strait of Hormuz, a major geopolitical chokepoint.

- Nearly 30% of LNG is used for fertilizer production, especially for ammonia and urea manufacturing.

- India’s urea consumption reached 387 lakh metric tonnes (2025), while domestic production stood at 306 lakh metric tonnes, indicating a supply gap.

- India imported over 2,300 lakh metric tonnes of urea, with 71% sourced from West Asia:

- 45% from Oman

- 26% from Saudi Arabia, Qatar, and UAE

- Urea plants are already operating at reduced capacity due to LNG supply disruptions.

Strategic Importance of LNG–Urea Linkage

- Natural gas is the primary feedstock for ammonia production, which is essential for urea manufacturing.

- Shift from naphtha and fuel oil to natural gas reflects India’s move towards cleaner and cost-efficient fertilizer production.

- Urea is the most widely used fertilizer in India, making it critical for agricultural productivity and food security.

- Thus, disruptions in LNG supply directly translate into risks for agricultural output and rural livelihoods.

Key Challenges

- Geopolitical Vulnerability: Heavy reliance on West Asia exposes India to conflicts, chokepoints like Strait of Hormuz, and supply disruptions.

- Dual Import Dependence: India depends on imports for both input (LNG) and final product (urea), increasing systemic risk.

- Supply Chain Disruptions: Force majeure declarations and reduced LNG cargoes have led to cutbacks in gas supply and plant operations.

- Energy–Agriculture Link Risk: Any energy shock now directly affects fertilizer availability and farm output, increasing economic vulnerability.

- Price Volatility: Global crises lead to higher LNG and crude prices, raising subsidy burden and fiscal stress.

Government Response

- The Natural Gas (Supply Regulation) Order, 2026 has prioritised the fertilizer sector in gas allocation.

- India has built urea reserves of 61.51 lakh metric tonnes (March 2026), higher than the previous year, to prepare for the Kharif season.

- State-owned companies like GAIL, IOC, and BPCL are managing supply curtailments amid disruptions.

Way Forward

- Diversification of Energy Sources: Reduce dependence on West Asia by sourcing LNG from multiple geographies and increasing domestic gas production.

- Strengthening Domestic Capacity: Enhance self-reliance in urea production through expansion of gas-based fertilizer plants.

- Strategic Reserves: Build buffer stocks of LNG and fertilizers to manage short-term disruptions.

- Alternative Fertilizers: Promote nano-urea, organic fertilizers, and balanced nutrient use to reduce dependence on conventional urea.

- Supply Chain Security: Develop secure maritime routes and strategic partnerships to safeguard energy and fertilizer imports.

Conclusion

- India’s fertilizer security is deeply intertwined with its energy security. The West Asia crisis exposes how geopolitics can directly affect agriculture and food systems. A resilient strategy must focus on diversification, domestic capacity building, and technological alternatives, ensuring that Indian farmers are protected from global uncertainties.