Context

- The European Union’s Carbon Border Adjustment Mechanism (CBAM) became fully operational on January 1, 2026, introducing carbon-linked charges on imports such as steel, aluminium, and cement. While positioned as a mechanism to ensure fair competition and prevent carbon leakage, CBAM has significant implications for India’s export competitiveness and climate policy autonomy.

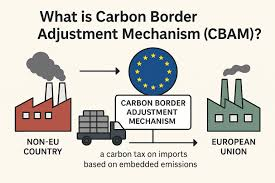

Understanding CBAM

- CBAM seeks to align the carbon cost of imports with that borne by European producers under the Emissions Trading System (ETS).

- Importers are required to pay for the embedded carbon emissions in imported goods, with adjustments permitted if a carbon price has already been paid in the country of origin.

- The mechanism currently targets carbon-intensive sectors, signalling the emergence of climate-linked trade regulation in global markets.

- Thus, CBAM represents a structural shift towards integrating environmental costs into international trade regimes.

Structural Asymmetry and Trade Concerns

- European industries continue to benefit from decarbonisation subsidies, concessional public finance, and free ETS allowances (phased out between 2026–2034).

- In contrast, Indian exporters face full CBAM liabilities without comparable fiscal or policy support, creating an uneven competitive landscape.

- This asymmetry raises concerns regarding consistency with GATT Article III, which prohibits discriminatory internal taxation favouring domestic producers.

- The India-EU FTA (2026) does not provide exemptions from CBAM, limiting India’s immediate negotiating leverage.

Core Issue

- CBAM effectively shifts part of Europe’s decarbonisation burden onto developing country exporters, without sharing associated financial resources.

- Revenues generated from carbon pricing are retained within the EU, raising concerns of inequitable burden-sharing.

- Countries lacking control over carbon pricing on their exports risk becoming rule-takers rather than rule-makers in global climate governance.

India’s Existing Framework: Carbon Credit Trading Scheme (CCTS)

- India’s Carbon Credit Trading Scheme (2023) establishes a domestic carbon market through tradable emission certificates linked to measured emissions.

- The scheme is expected to expand across energy-intensive sectors, including steel and manufacturing.

- Under CBAM Regulation Article 9, carbon prices paid domestically can be credited against CBAM obligations, providing a legal pathway for recognition of India’s system.

- Strategic Response: India Border Adjustment Mechanism (IBAM)

- India may consider introducing an India Border Adjustment Mechanism (IBAM), imposing a domestic carbon charge on exports aligned with CBAM requirements.

- The design must be developed through FTA Annex 14-A technical dialogue, ensuring international recognition under CBAM Article 9.

- Proper sequencing would ensure that Indian exporters face no additional net carbon burden, while shifting revenue collection from the EU to India.

Economic and Developmental Implications

- Retaining carbon revenues within India can support green industrial transformation and technological upgrading.

- Potential utilisation includes:

- Modernisation of carbon-intensive industries (e.g., steel)

- Expansion of renewable energy and green hydrogen

- Support for labour transition and skill development

- Transparent and ring-fenced utilisation of funds is essential to ensure credibility, efficiency, and public trust.

Way Forward

- Leverage Legal Provisions: Actively utilise CBAM Article 9 and FTA Annex 14-A to secure recognition of domestic carbon pricing.

- Develop IBAM with Caution: Ensure compliance with international trade rules and avoid unilateral measures that may trigger disputes.

- Strengthen Domestic Carbon Markets: Expand the scope, transparency, and credibility of CCTS implementation.

- Promote Climate Diplomacy: Advocate for equitable global carbon frameworks recognising differentiated responsibilities.

- Align Trade and Climate Policy: Integrate carbon pricing with industrial policy, export competitiveness, and energy transition strategies.

Conclusion

- CBAM marks a decisive shift in global trade, embedding climate considerations into market access and competitiveness frameworks. India’s response must ensure that climate action does not compromise economic sovereignty or developmental priorities. By strategically leveraging domestic policy instruments, India can ensure that its carbon revenues are retained and reinvested in its own green transition, thereby aligning climate responsibility with national interest.