Context

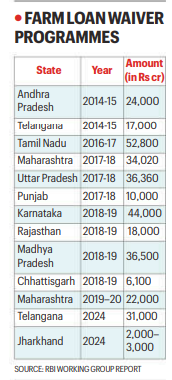

- The Maharashtra government announced a ₹35,000 crore farm loan waiver scheme, ignoring caution from RBI and several working groups against such waivers.

- Since FY15, 10 states have announced loan waiver programmes of an aggregate amount of ₹2.4 lakh crore (1.4% of 2016-17 GDP at current prices), significantly higher than the two previous nationwide debt waiver programmes.

- Central and state governments have spent a whopping ₹3.5 lakh crore in the last 35 years on farm loan waivers, yet only 50% of 3.7 crore eligible farmers benefited.

Stated Rationale

- Alleviate debt overhang of beneficiaries, enabling productive investment and boost real economic activity.

- States like Karnataka expanded loan waivers from ₹18,000 crore (FY18) to ₹44,000 crore (3.4% of GSDP) in FY19.

- Madhya Pradesh and Chhattisgarh announced new loan channels worth 1.9% and 1.7% of state GSDP respectively.

Impact of Farm Loan Waiver

- Fiscal Impact on States

- Fiscal burden on states’ budgets is typically staggered over 3-5 years through phased rollouts or clearing bank dues over multi-year pay-outs.

- Impact varies widely across states, ranging between 0.1% of GSDP (Andhra Pradesh and Tamil Nadu) to 1.8% of GSDP (Chhattisgarh in FY19).

- In FY20, states have allocated between 0.2% and 1.8% of GSDP to farm loan waivers.

- Impact on Credit Culture (RBI’s Concerns)

- Sharp deceleration in agricultural credit growth and declined agricultural credit disbursements observed in years following loan waiver programmes, with growth bouncing back in subsequent years.

- Waivers have adversely affected the credit history of borrowers and their future prospects of availing fresh loans for agricultural purposes.

- Many borrowers withhold repayment in anticipation of a loan waiver, thus directly undermining credit discipline.

- Gross NPA in the agriculture sector stood at 8.44% as on March 31, 2019, reflecting a high level of non-performing assets.

- In FY18 and FY19, all states that announced farm loan waivers showed either no material change in NPA levels or actually registered a decline, thus indicating the presence of moral hazard, with borrowers defaulting strategically in anticipation of waiver.

- RBI has discouraged loan waivers on various occasions, noting they affect credit culture and impact state finances adversely, harming farmers’ interests in the medium to long term.

Way Forward

- Targeted income support like PM-KISAN (₹6,000/year) is a more fiscally sustainable alternative to blanket loan waivers.

- Crop insurance strengthening through PM Fasal Bima Yojana reduces distress without moral hazard risks.

- Interest subvention schemes provide relief without undermining repayment culture or burdening state finances.

- Kisan Credit Cards (KCC) and institutional credit deepening can reduce dependence on moneylenders and prevent debt traps.

- Agricultural market reforms addressing MSP, procurement, and supply chain efficiency tackle root causes of farm distress rather than symptoms.