Context

- Despite launching a revamped disinvestment policy in 2021, the government’s focus has decisively shifted toward extracting maximum value from existing assets.

- PM Modi in 2021 asserted that the government has “no business to be in business”, signalling intent to minimise state presence in commercial activities.

- The recent launch of National Monetisation Pipeline 2.0 marks a clear extension of this policy direction.

Decline of Disinvestment Revenue

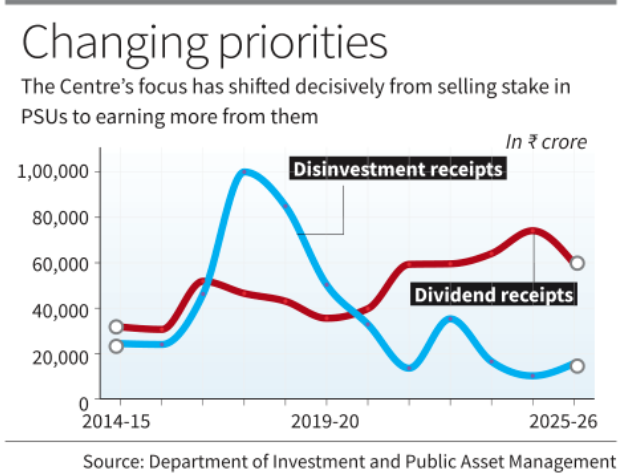

- Except for a brief surge in 2022-23 (₹35,294 crore), disinvestment revenue has been falling consistently every year.

- Revenue fell sharply to ₹16,507 crore in 2023-24 and further to ₹10,163 crore in 2024-25.

- The private sector showed little interest in buying PSUs due to large employee headcounts and loss-making assets.

- In 2023-24, the Centre removed the separate disinvestment header from Budget documents, clubbing it under ‘Miscellaneous Capital Receipts’.

- The government no longer sets annual disinvestment targets, marking a quiet but significant policy retreat.

Rise of Dividend-Based Revenue

- The government shifted focus to maximising dividends from Central Public Sector Enterprises ( CPSEs).

- DIPAM issued a consistent dividend policy advisory in 2020, directing CPSEs to pay higher dividends considering profitability and reserves.

- Revised Guidelines on Capital Restructuring (2024) emphasised creating value in CPSEs to maximise returns for government and shareholders.

- Dividend receipts from CPSEs (excluding banks and RBI) rose from ₹39,750 crore in 2020-21 to ₹74,128 crore in 2024-25, a near doubling.

Asset Monetisation: The New Strategy

- In 2021, the government launched the National Monetisation Pipeline (NMP) — leasing brownfield assets to the private sector without transferring ownership.

- NMP 1.0 target was ₹6 lakh crore (2021-25), with the government claiming 90% achievement.

- NMP 2.0 was launched in February 2025 with a target of ₹16.72 lakh crore over 2025-30 — nearly three times the earlier pipeline.

- Asset monetisation allows private sector efficiency without permanent loss of public assets — a middle path between privatisation and state ownership.

Implications and Way Forward

- The shift reflects a pragmatic acknowledgement that outright privatisation faces political and practical resistance in India’s economic landscape.

- Maximising dividends and monetising assets ensures fiscal revenue without permanently exiting public ownership.

- However, over-dependence on PSU dividends raises questions about long-term sustainability if PSU profitability declines.

- The success of NMP 2.0 depends on credible regulatory frameworks, investor confidence, and transparent leasing mechanisms.

- The broader question remains whether this shift represents a genuine reform vision or a tactical retreat from the original disinvestment ambition.

About Disinvestment

- What is Disinvestment?

- The process of reducing or liquidating government ownership in a company or asset through the sale of shares or assets

- Undertaken to raise capital, improve efficiency, or reduce government intervention in the economy

- Key Institutions

- Overseen by Department of Investment and Public Asset Management (DIPAM) under the Ministry of Finance

- National Investment Fund (NIF): Established in 2005 to serve as a channel for proceeds generated from disinvestment of Central Public Sector Enterprises (CPSEs)

- Approaches to Disinvestment

- Minority Disinvestment: Government retains more than 51% stakes thus retaining control.

- Majority Divestment: Hands over control but retains some stake

- Complete Privatisation: 100% control transferred to private parties

- Methods of Disinvestment

- Initial Public Offering (IPO): Shares offered by an unlisted PSE to the public for the first time

- Further Public Offering (FPO): Shares offered by a listed PSE to the public for subscription

- Offer for Sale (OFS): Auction of shares by promoters through the Stock Exchange platform — extensively used by the Government since 2012

- Strategic Sale: Sale of a substantial portion of government shareholding (up to 50%) along with transfer of management control

- Institutional Placement Programme (IPP): Only Qualified Institutional Buyers (QIBs) can participate, perceived to possess expertise in capital markets

- CPSE Exchange Traded Fund (ETF): Allows simultaneous sale of government’s stake in various PSEs across diverse sectors through a single offering