India’s Energy Security: LPG, LNG, and Strategic Reserves

Context and Impact of Crisis

- Disruption in the Strait of Hormuz due to the West Asia conflict has affected India’s energy supplies.

- India imports ~60% of LPG, and ~90% passes through the Strait, leading to ~54% supply disruption.

- Around 50% of natural gas is imported as LNG, with 30% supply disruption.

- The government prioritised household consumption, reducing supply to industrial and commercial users.

- The LPG situation is more difficult than LNG, prompting a shift towards PNG.

Properties of LPG and LNG

- LPG: Mixture of propane and butane, derived from crude oil refining and gas processing.

- LNG: Primarily methane, derived from natural gas.

- Liquefaction:

- LPG: Liquefied under moderate pressure/low temperature.

- LNG: Requires cryogenic cooling below -160°C.

- Volume Reduction:

- LPG: Reduced to 1/260th of gaseous volume.

- LNG: Reduced to 1/600th, enabling long-distance transport.

- Safety:

- LPG: Heavier than air, accumulates and increases explosion risk.

- Natural gas (PNG): Lighter than air, disperses quickly.

Usage, Distribution and Accessibility

- LPG Uses: Cooking, heating, industrial applications, and limited transport use.

- LNG Uses: Transported and converted to natural gas for PNG, CNG, fertilisers, power, refineries, petrochemicals.

- Distribution:

- LPG: Delivered in cylinders via road, suitable for remote areas.

- LNG: Transported via cryogenic ships → regasification → pipelines.

- Accessibility:

- LPG: Portable and widely accessible, especially in rural areas.

- PNG: Depends on pipeline infrastructure, mainly urban areas.

- Convenience:

- PNG: Continuous supply, no refill required.

- LPG: Requires periodic cylinder replacement.

Government Response and Policy Measures

- Supply prioritisation:

- 100% supply ensured for households (PNG/CNG).

- Industrial/commercial supply reduced to ~80%.

- User base:

- LPG: 33.3 crore households

- PNG: 1.5 crore connections

- PNG promotion:

- Incentives like free gas and waived connection charges.

- Push for City Gas Distribution (CGD) expansion.

- Domestic LPG production:

- Increased by 40%, share rose to ~55% of demand.

- Demand management:

- Booking gap increased to 25 days (urban) and 45 days (rural).

- Alternative fuels:

- Use of kerosene, fuel oil, biomass, coal for industries.

Dengue Vaccine Qdenga (TAK-003): Features, Efficacy, and India Launch

About

- Qdenga (TAK-003) is a live-attenuated tetravalent dengue vaccine developed by Takeda Pharmaceuticals.

- It targets all four dengue virus serotypes: DENV-1, DENV-2, DENV-3, and DENV-4.

- Built on a DENV-2 genetic backbone, with components of other serotypes integrated.

- Designed to provide broad protection against dengue infection.

Features and Mechanism

- Being live-attenuated, it uses weakened viruses to stimulate immune response.

- Provides protection against severe dengue and hospitalization.

- Does not require prior dengue infection screening, unlike earlier vaccines.

- Suitable for both seropositive and seronegative individuals.

Efficacy and Dosage

- Demonstrates long-term protection (more than 4 years).

- Shows over 80% reduction in dengue-related hospitalisation.

- Administered in a two-dose schedule, with a 3-month interval between doses.

Global and India Context

- Received WHO prequalification in May 2024, enabling wider global use.

- Recommended for individuals aged 4 to 60 years.

- In India:

- Expected launch by 2026.

- The Subject Expert Committee (SEC) has recommended its import and marketing.

- Manufactured in partnership with Biological E (Hyderabad).

- Supports Make in India by enhancing domestic vaccine production and accessibility.

Commodity Derivatives Trading in India: NCDEX, MCX, and Price Risk Management

Meaning and Basic Concept

- Derivatives are short-term financial contracts traded in markets.

- Their value is derived from an underlying asset, such as agricultural commodities.

- Profit is earned by predicting price movements of the underlying commodity.

Types of Derivative Contracts

- Futures Contract:

- A seller agrees to sell a fixed quantity at a predetermined price on a future date.

- Creates a binding obligation for both buyer and seller.

- Options Contract:

- Gives the buyer the right, but not the obligation, to buy or sell an asset.

- Provides flexibility with limited risk compared to futures.

Role in Agriculture and Price Risk Management

- Farmers can lock in prices for their produce by entering into derivative contracts.

- Commodities must meet exchange-specified quality standards.

- Acts as a form of price insurance, protecting against market fluctuations.

Trading Mechanism and Exit

- Contracts can be bought and sold before expiry in the market.

- Traders or producers can exit positions by paying a margin to the exchange.

- Helps in maintaining liquidity and flexibility in trading.

Commodity Exchanges in India

- Major platforms for commodity derivatives trading:

- National Commodity and Derivatives Exchange (NCDEX)

- Multi Commodity Exchange (MCX)

- Commonly traded agricultural commodities include: Cotton, paddy, soybean, soya oil, mustard seed, etc.

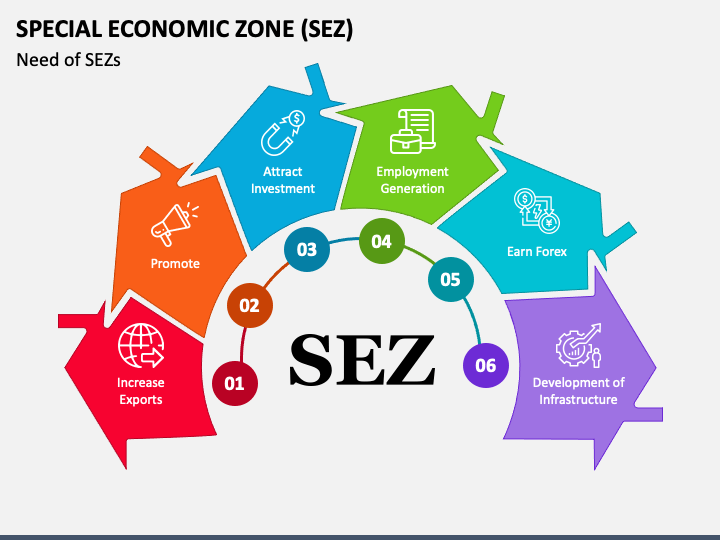

Special Economic Zones (SEZs) in India: SEZ Act 2005, Incentives, and 2025 Amendments

Concept and Objectives

- SEZs are designated areas within a country offering special economic regulations and incentives for businesses.

- They provide duty-free trade, tax benefits, and world-class infrastructure to promote ease of doing business.

- Key objectives include:

- Promoting exports of goods and services

- Attracting foreign and domestic investment

- Generating employment opportunities

- Boosting economic activity and infrastructure development

- SEZ category includes various forms such as:

- Free Trade Zones (FTZs)

- Export Processing Zones (EPZs)

- Free Ports and Industrial Estates

Evolution and Status in India

- Asia’s first Export Processing Zone (EPZ) was set up at Kandla (1965).

- SEZ Policy was introduced in April 2000 to make SEZs engines of economic growth.

- SEZ Act, 2005, passed; came into force on February 10, 2006 (with SEZ Rules).

- Existing EPZs converted into SEZs (e.g., Kandla, Surat, Mumbai, Cochin, Chennai, Visakhapatnam, Falta, Noida).

- As of March 31, 2024: 280 operational SEZs in India.

Key Features and Incentives

- SEZ is treated as a duty-free enclave, considered outside customs territory for authorised operations.

- Duty-free import and domestic procurement are allowed for SEZ units.

- No import licence required; both manufacturing and services permitted.

- Tax Incentives (Section 10AA):

- 100% exemption on export income for first 5 years

- 50% for next 5 years

- 50% of reinvested export profits for next 5 years

- GST Treatment:

- Supplies to SEZs are zero-rated under IGST Act, 2017.

- Operational Flexibility:

- Single-window clearance for approvals

- Subcontracting allowed

- No routine customs inspection for cargo

- Compliance Requirements:

- Must maintain Positive Net Foreign Exchange (NFE) over 5 years

- Domestic sales allowed but subject to customs duties

- Minimum Alternate Tax (MAT) applicable

2025 Amendments

- Focus on promoting semiconductor and electronic component manufacturing.

- Rule 5 amended: Minimum land requirement reduced from 50 hectares to 10 hectares.

- Rule 18 amended: SEZ units allowed to sell in domestic market on payment of applicable duties.

- Rule 7 amended: Board of Approval empowered to relax encumbrance-free land requirement in specific cases (e.g., mortgaged/leased land).

Foreign Contribution (Regulation) Amendment Bill, 2026

Context and Purpose

- The proposed FCRA Amendment Bill, 2026 seeks to strengthen regulation of foreign funds received by NGOs and individuals.

- It aims to address regulatory gaps, accountability issues, and misuse of foreign contributions.

- The parent law is the Foreign Contribution (Regulation) Act, 2010, administered by the Ministry of Home Affairs (MHA).

Key Provisions of Amendment Bill, 2026

- Designated Authority for Assets:

- The government can appoint an authority to take over, manage, or dispose assets created from foreign funds.

- Proceeds may be transferred to the Consolidated Fund of India.

- Expanded “Key Functionary” Definition:

- Includes directors, trustees, partners, karta (HUF), office-bearers, etc.

- Such persons can be held personally liable for violations.

- Prior Approval for Investigation:

- State governments and law enforcement agencies must obtain Central Government approval before initiating FCRA-related investigations.

- Timelines and Automatic Cessation:

- Fixed timelines for receipt and utilisation of funds.

- Registration will automatically lapse if not renewed.

- Reduced Punishment:

- Maximum imprisonment reduced from 5 years to 1 year, with rationalised penalties.

FCRA Act, 2010: Core Features

- Regulates acceptance, utilisation, and accounting of foreign contributions and hospitality.

- Came into force in 2011; amended in 2016, 2018, and 2020.

- Around 16,000 registered associations, receiving ~₹22,000 crore annually.

- Objective:

- Prevent use of foreign funds for activities against national interest, sovereignty, and public order.

- Registration Requirements:

- Mandatory registration or prior permission from Central Government.

- Valid for 5 years, renewal required before expiry.

- Organisation must:

- Be registered under relevant laws

- Have minimum 3 years track record

- Spend at least ₹15 lakh in last 3 years

- Banking Rule:

- Foreign funds must be received in a designated SBI account (New Delhi main branch).

- Utilisation Restrictions:

- No transfer (sub-granting) to unregistered entities.

Restrictions and Prohibitions

- Foreign contribution prohibited for:

- Election candidates

- Journalists and media entities

- Judges and government servants

- Members of legislature

- Political parties and organisations of political nature

- Applicants must not:

- Be fictitious entities

- Be involved in communal disharmony or anti-national activities

General Anti-Avoidance Rules (GAAR): Concept, Features, and Tax Avoidance

Concept

- GAAR is an anti-tax avoidance framework under the Income Tax Act, 1961.

- It came into effect from 1st April 2017.

- It aims to curb aggressive tax planning that leads to revenue loss for the government.

- Targets arrangements that are legally valid in form but designed to avoid tax in substance.

Key Features

- Applies to transactions or arrangements primarily undertaken to reduce tax liability.

- Focuses on substance over form, i.e., the real intention behind the transaction.

- Designed to tackle tax avoidance, not legitimate tax planning.

- Covers cases where:

- Arrangement lacks commercial substance

- The main purpose is the tax benefit

- Structure is artificial or contrived

Powers under GAAR

- Tax authorities can declare a transaction as an Impermissible Avoidance Arrangement (IAA).

- They can:

- Re-characterise or disregard transactions

- Recompute income and tax liability

- Deny tax benefits arising from such arrangements

Procedural Aspect and Threshold

- Applicable to cases involving significant tax impact.

- Reassessment notices for under-reported income of ₹50 lakh or more can be issued within:

- 5 years and 3 months from the end of the relevant assessment year.

Copyright Act 1957: Fair Dealing, Duration, and International Conventions

Background and Purpose

- The Copyright Act, 1957 is the first post-independence copyright law in India, replacing the 1914 Act.

- It aligns India with international conventions such as:

- Berne Convention (1886)

- Universal Copyright Convention (1951)

- Rome Convention (1961)

- TRIPS Agreement

- India also joined the WIPO Copyright Treaty (WCT) and the WIPO Performances and Phonograms Treaty (WPPT) in 2013, strengthening digital copyright protection.

- The Act grants creators exclusive rights such as:

- Reproduction, adaptation, distribution, translation, and communication to the public.

Key Provisions and Features

- Copyright is a bundle of rights covering:

- Reproduction, communication, translation, adaptation

- Covers a wide range of works:

- Literary, musical, dramatic, artistic works

- Cinematograph films and sound recordings

- Includes software, databases, architecture, and craftsmanship

- Ownership and Assignment:

- Author is the first owner, except in employer-employee cases

- Assignment must be through a written agreement (Section 19)

- If duration not specified → valid for 5 years

- If territory not specified → limited to India

- Recognises joint authorship when contributions are indistinguishable.

- Provides civil, criminal, and administrative remedies (including customs detention).

- Jurisdiction based on the place where cause of action arises (as per Supreme Court ruling).

- Foreign works protected via International Copyright Order.

Exceptions (Fair Dealing – Section 52)

- Ensures balance between creator rights and public interest.

- Permitted uses include:

- Private use and research

- Education and teaching

- Criticism and review

- Reporting of current events

- Freedom of Panorama:

- Allows photography/depiction of buildings and public artworks

- Permits inclusion of such works in films if incidentally present

Duration of Copyright

- Literary, dramatic, musical, artistic works: Lifetime of author + 60 years after death

- Other categories (60 years from publication):

- Cinematograph films

- Sound recordings

- Photographs

- Government works

- Public undertakings and international organisations

- Anonymous/Pseudonymous works: 60 years from publication

- For foreign works, duration cannot exceed country of origin.