Context: India’s retail inflation appears stable at 3.4%, but underlying trends reveal deeper inflationary pressures driven by external and structural factors.

Understanding the Inflation Paradox

- The current inflation situation appears deceptively benign, as headline CPI remains within the RBI’s tolerance band.

- However, a sharp rise in Wholesale Price Index (3.88%, 38-month high) signals growing cost pressures at the producer level.

- The divergence between CPI and WPI reflects a lag in transmission of input costs to consumers.

- This creates a temporary illusion of stability while underlying inflationary pressures continue to build.

Drivers of Emerging Inflationary Pressures

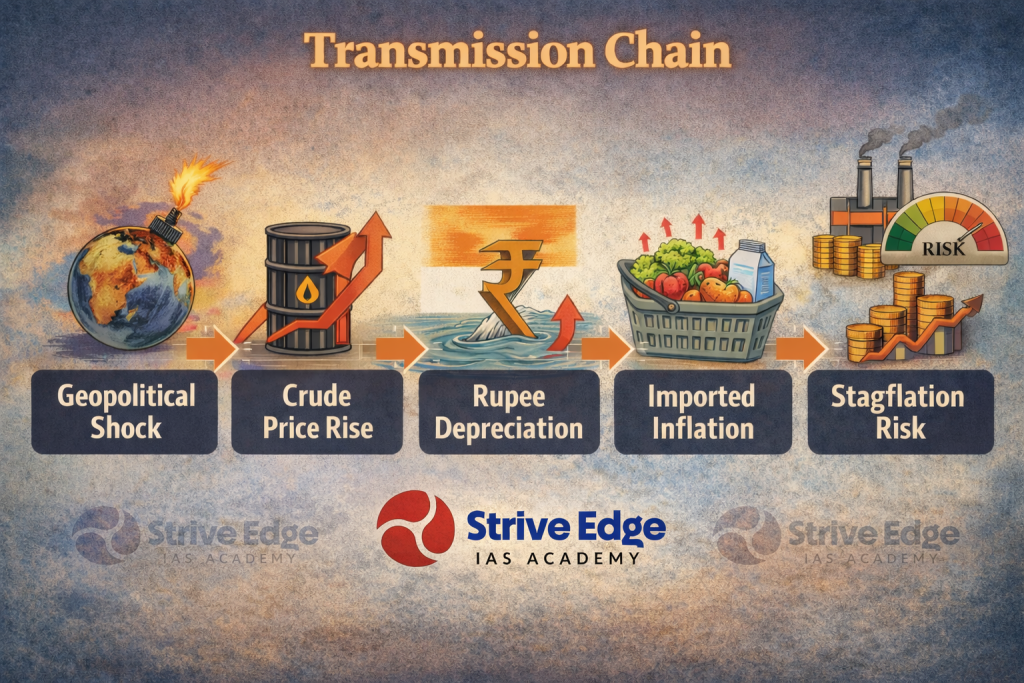

- Imported inflation through currency depreciation: A 2.5–3% fall in rupee value has increased the cost of dollar-denominated imports like crude oil and gas.

- Energy price shocks: Geopolitical tensions (U.S.-Israel-Iran conflict) have disrupted supply chains, pushing up global fuel prices.

- Input cost escalation: Rising prices of fertilizers, petrochemicals, and plastics are increasing costs across pharmaceutical, textile, and automobile sectors.

- Supply chain disruptions: Decline in exports and imports reflects not weak demand but war-induced disruptions in global trade flows.

- Domestic supply distortions: MSMEs are redirecting exports to domestic markets, creating temporary supply gluts and suppressing consumer prices.

Hidden Faultlines

- Suppressed inflation dynamics: Firms are absorbing rising input costs, delaying price transmission to consumers, which masks real inflationary pressures.

- Artificial price stability: Domestic supply gluts due to export diversion are keeping retail inflation temporarily low, creating a false sense of stability.

- Producer distress: While CPI remains controlled, rising costs are compressing profit margins and financial sustainability of firms.

- Stagflationary risk emerging: As cost pressures pass through, inflation may rise alongside slowing growth, creating a potential stagflation scenario.

- External growth signals: Global slowdown indicators and reduced growth projections highlight weakening economic momentum.

- Energy dependence vulnerability: Heavy reliance on imported fossil fuels exposes India to global price shocks and currency fluctuations.

- Imported inflation trap: Oil-import dependence amplifies inflation through exchange rate depreciation and global supply disruptions.

Way Forward

- Accelerate energy transition: Shift towards renewable energy to reduce dependence on volatile global fuel markets.

- Strengthen macroeconomic resilience: Manage currency volatility and diversify import sources.

- Improve supply chain efficiency: Reduce transmission delays and distortions in price signals.

- Support MSMEs: Provide buffers against cost shocks to prevent margin compression and job losses.

- Balanced policy response: Combine inflation control with growth support to avoid stagflationary traps.

Conclusion

- India’s current inflation appears stable on the surface but hides structural vulnerabilities and external risks. A forward-looking approach focused on energy transition and macroeconomic resilience is essential to ensure sustainable and stable growth.